Avoiding the Trap: Common Legal Pitfalls in Business Sales

Finding the right buyer is often the primary focus for business owners looking to sell. However, focusing solely on the buyer while overlooking the legal framework of the transaction is a risky strategy. Legal missteps can delay or even derail a business sale, potentially leading to significant financial losses.

At First Choice Business Brokers of the Triangle, we believe that legal preparation is just as important as pricing your business correctly. Here is a guide to the most common pitfalls and how to navigate them to ensure a secure, efficient sale.

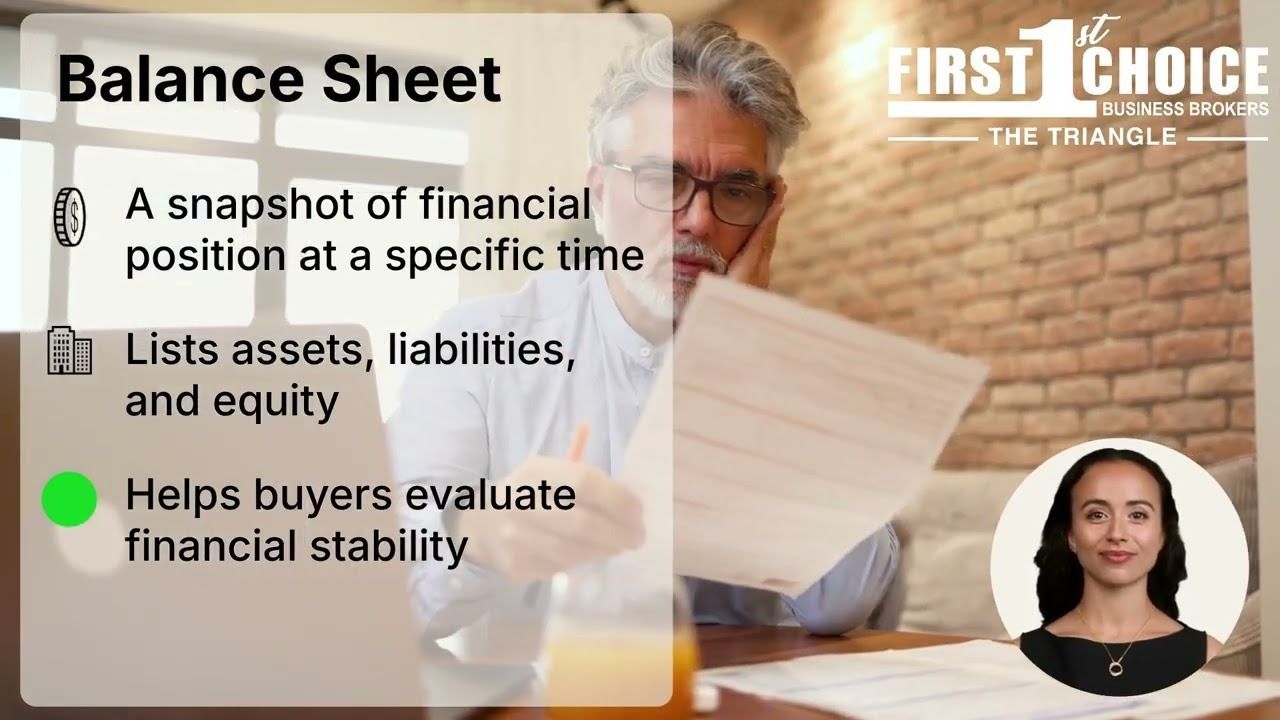

The Importance of Documentation

Buyers expect a well-documented business. When you enter the market, you must have clear financials, contracts, and legal records ready for review.

Missing or disorganized paperwork can cause delays or raise doubts about the credibility of your business. Before listing, ensure all your records are accurate, up-to-date, and easily accessible. This organization builds trust and keeps momentum in the deal.

Solidifying the Sales Agreement

A handshake isn't enough. A weak or unclear sales agreement often leads to disputes long after the sale is complete. To avoid misunderstandings, the agreement must clearly outline the terms, including assets, liabilities, and payment structure.

We strongly recommend working with a business attorney to ensure the contract fully protects your interests and leaves no room for ambiguity.

Transparency and Liabilities

It can be tempting to downplay the negatives, but failing to disclose legal or financial liabilities can damage trust or even cancel the sale.

Buyers will almost certainly discover these issues during the due diligence phase. Being upfront and addressing liabilities beforehand will strengthen your position, proving that you are an honest operator with nothing to hide.

Protecting Confidentiality

Prematurely revealing a sale can disrupt your operations. If you don't require buyers to sign a non-disclosure agreement (NDA) before sharing financials, you may unintentionally alert customers, employees, and competitors to the sale. This can destabilize your business right when you need it to remain strong.

Additionally, a well-drafted non-compete clause is standard practice to assure the buyer that you won't immediately start a rival company after closing.

Planning for Taxes

It’s not just about what you sell for; it’s about what you keep. Failing to plan for capital gains taxes or outstanding obligations can create unforeseen financial burdens.

Consulting with a tax professional or wealth advisor ensures you are prepared for the tax implications of a financial windfall, maximizing the final amount you take home.

Navigate with Confidence

Legal pitfalls can complicate your business sale, but with the right preparation, you can avoid costly mistakes. At First Choice Business Brokers of The Triangle, we help sellers navigate legal and financial complexities and maximize their business's value.

If you are ready to prepare your business for a successful exit,

contact us today for expert guidance and a no-cost business valuation.

Disclaimer: This content is for informational purposes only and does not constitute legal or tax advice. Consult qualified professionals regarding your specific situation.

Recent articles for you